Personal Finance Tips: A Beginner’s Guide to Budgeting, Saving, and Managing Money

Key Takeaways

Personal finance tips help you create a simple budget, save money consistently, manage debt, and build an emergency fund—essential skills in 2026's high-cost environment with inflation around 3-4% and credit card APRs averaging 24.5%.

Small, steady steps make a real difference: tracking spending for 30 days and automating $25-$50 in monthly savings can significantly improve your financial stability within a few years.

Avoiding high interest debt (often above 20% APR) and building a 3-6 month emergency fund should be your core priorities as a beginner.

You don't need a high income to get started—the same principles work whether you earn $30,000 or $100,000 annually.

You can take control of your money today by setting one clear financial goal and making a simple action plan for this week.

What Are Personal Finance Tips? (Beginner Overview)

Personal finance tips are practical, everyday strategies for budgeting, saving, managing debt, and setting goals that help you take control of your money. These aren’t complex investment schemes—they’re simple habits anyone can build.

Financial literacy matters more than ever in 2026. With inflation hovering around 3-4% annually, rent increasing 5-7% year-over-year in major cities, and average credit card APRs hitting 24.5%, understanding how to manage your income and expenses is essential for staying afloat.

The core areas of personal finance include:

Creating a budget to track where your net income goes each month

Tracking income and expenses to spot spending leaks

Saving money consistently to counter inflation’s effects

Managing debt to avoid compounding interest burdens

Building credit through on-time payments

Planning for goals like retirement or homeownership

These fundamentals build financial stability by helping you pay bills on time, avoid overdraft fees (which cost Americans $11 billion yearly), and work toward long-term wealth through investing and smart financial decisions.

Why Managing Your Money Is Important

Good money management provides security, reduces stress, and opens doors. Research from the American Psychological Association shows that financial control can reduce chronic stress by up to 30%. When you manage your finances well, you gain choices—the ability to change jobs, move cities, or handle emergencies without panic.

Poor spending habits create real barriers. The average U.S. household overspends $237 monthly on subscriptions alone, according to a 2025 Rocket Money report. Add frequent food delivery, impulse purchases, and high interest debt on credit cards, and you’re looking at thousands annually that could have funded an emergency savings account or paid down student loans.

Strong money management delivers tangible benefits:

Avoiding $35 average overdraft fees per incident

Boosting credit scores above 700 for better loan terms

Covering a $1,000 emergency without going into debt

Making progress toward retirement savings with employer match contributions

The connection between money mindset and financial success is real. Studies show that disciplined savers with modest $50,000 incomes often outperform impulsive high-earners over decades. When you view money as a controllable tool rather than something that “just disappears,” you unlock the ability to build more money over time through consistency.

Personal Finance Tips for Beginners

This is the main “how-to” section with practical personal finance tips you can implement immediately. You don’t need to apply every tip at once—start with one or two, like creating a monthly budget and building a starter emergency fund of $500, then expand over time.

The following subsections break down specific beginner tips, each with concrete actions you can start within the next week.

1. Create a Simple Budget

A budget is a plan for where every dollar of your monthly income goes. It eliminates the mystery of where your paycheck disappeared.

Start with personal budgeting basics: list all income sources for the month (salary, side gigs, child support) against all fixed expenses (rent, utilities, car payment) and variable expenses (groceries, subscriptions, transport).

How to get started:

A straightforward method is the 50/30/20 rule: allocate 50% to needs, 30% to wants, and 20% to savings and debt payments. On a $4,900 monthly income, that’s roughly $2,450 for essentials, $1,470 for discretionary spending, and $980 for financial goals.

Keep your budget flexible. Revisit it weekly at first—rigid plans have a 40% failure rate compared to adaptive ones.

2. Build Better Spending Habits

Daily money choices—coffee runs, food delivery, online shopping—compound into major impacts on your finances. A $5 daily coffee habit costs $1,825 annually.

Start by reviewing 1-3 months of bank statements and credit card statements. Look for patterns: frequent takeout, unused subscriptions, or impulse purchases. Research shows 40% of purchases are later regretted.

Tips to reduce monthly expenses:

Plan weekly meals and cook at home to save $200-300 monthly on food delivery

Use public transit over rideshares to save approximately $100/month

Set a 48-hour waiting period before nonessential purchases over $50

Cancel unused subscriptions (the average household has $237 in monthly subscription waste)

Replace expensive habits with free alternatives like library resources or community events

Tracking spending for even one month reveals patterns you didn’t know existed. Most people discover $100-200 in spending they don’t miss cutting.

3. Start Saving Money Consistently

Starting to save in 2026—even small amounts like $25-$100 per month—matters because inflation erodes purchasing power over time. Money sitting in a checking account loses value, while a high-yield savings account earning 4.5-5% APY helps your savings grow.

Easy ways to save money each month:

Treat savings like a bill in your budget—non-negotiable

Redirect canceled subscriptions directly into a savings account

Deposit part of tax refunds or bonuses (average federal refund is $2,800)

Use round-up features to save spare change automatically

Automate your saving by setting up a direct deposit split or scheduled transfers on payday. When saving happens before spending, you remove the decision-making friction. Fidelity data shows users who automate save 70% more than those who don’t.

Start with 5% of income and increase by 1-2% every 3-6 months. Consistency over years matters far more than perfection in any single month.

4. Set Clear Financial Goals

Money needs a purpose. Clear savings goals guide everyday decisions and reduce the stress of wondering if you’re doing enough.

Short-term goals (0-2 years):

Building a $1,000 emergency buffer

Paying off a small credit card

Saving for a 2027 vacation

Long-term goals (5+ years):

Saving for retirement in a 401 k or IRA

Building a home down payment

Achieving debt freedom

Write down 3-5 goals with target amounts and dates. For example: “Save $3,000 for emergency savings by June 2027.” This specificity creates focus and helps you decide where extra money should go.

Align goals with your values. If flexibility matters, prioritize eliminating debt. If family security is paramount, focus on emergency funds first. A wealth building mindset emphasizes patience and consistent investing over get-rich-quick schemes.

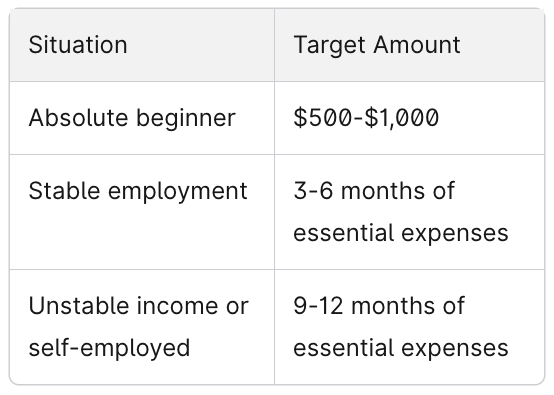

5. Build an Emergency Fund

An emergency fund is cash set aside for genuine emergencies—job loss, medical bills, or unexpected car repairs. It’s not for vacations or gifts.

Emergency fund targets by situation:

Keep your emergency fund in an FDIC-insured high-yield savings account separate from your everyday checking account. This separation prevents accidental spending while keeping funds accessible when needed. Current top rates from institutions like Ally and Synchrony offer 4.5-5%+ APY.

To build your fund faster, direct tax refunds, work bonuses, or side-hustle income entirely toward this account. Even $50/month adds up to $600 in a year—enough to cover many common emergencies without credit card debt.

A 2025 Bankrate survey found that 60% of Americans couldn’t cover a $1,000 emergency without going into debt. Building this buffer is foundational to financial stability.

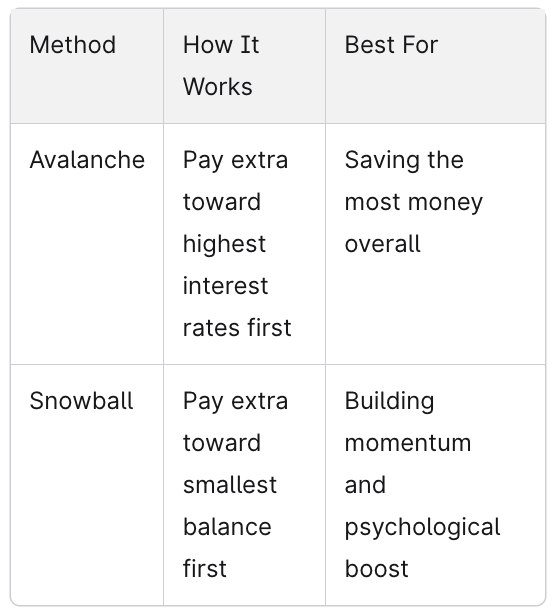

6. Manage Debt Effectively

Managing debt is crucial when many credit card APRs exceed 24%. Paying only minimums on a $6,000 balance could take 20+ years and cost $15,000 in interest.

Start with basics: list all debts including investment accounts, personal loans, auto loans, and student loans. Note each balance, interest rate, and minimum payment.

Two proven payoff strategies:

Always make at least minimum payments on every account to protect your credit score. Avoid taking on new high interest debt whenever possible.

Consolidating debt into a lower-rate option through a credit union or bank may help some people, but compare fees (typically 3-5%) and read terms carefully before committing.

Budgeting and Saving Tips That Actually Work

Budget creating and saving are ongoing processes that must adapt as life changes. A plan that worked at 25 may need adjustments at 30 when you have different income sources, housing costs, or family obligations.

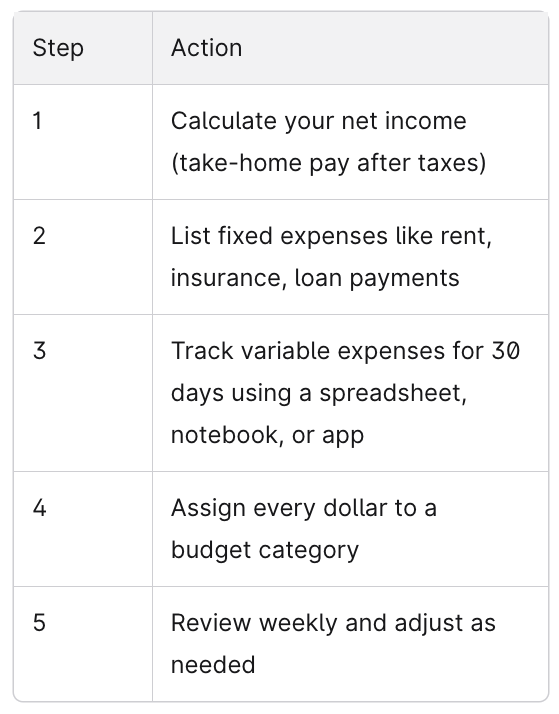

How to budget your money step by step:

Calculate take-home pay from all income sources

List all bills and fixed expenses first

Estimate variable expenses based on 3 months of data

Assign spending limits to each budget category

Ensure positive cash flow (income minus expenses equals savings)

Balancing cash flow means your monthly income reliably covers essentials, minimum debt payments, and at least a small amount of savings. If you’re spending more than you earn, identify one expense to reduce before the month ends.

Practical tips for consistency:

Schedule a monthly “money check-in” for 15 minutes

Use calendar reminders for bills to avoid late fees

Round up purchases to the nearest dollar and save the difference

Review your plan every 3 months or after major life stages changes

Smart Money Habits to Improve Your Finances

Habits—small actions repeated over time—are more powerful for personal finance than one-time big efforts. Building strong financial habits creates automatic progress toward your goals.

Financial habits worth building:

Pay bills on time, every time

Review your checking and savings accounts weekly

Save a set amount each pay period before spending

Limit high interest debt use to emergencies only

Check your credit report quarterly to spot errors

Improve financial discipline by removing friction for good habits and adding friction for bad ones. Set up automatic transfers for savings. Delete stored credit card information from shopping sites to reduce impulse purchases by up to 30%.

Develop a long-term money management strategy that sequences priorities: emergency fund first, then high-interest debt payoff, then start investing. Vanguard research shows that consistent adherents to basic plans can double their net worth over 5-10 years.

Review your financial habits annually—perhaps each January—to reset goals and assess how far you’ve come over the previous 12 months.

Common Personal Finance Mistakes to Avoid

Avoiding common mistakes can be just as powerful as following good personal finance tips. Here’s what to watch for.

Overspending without a budget: A 2026 LendingClub report found 63% of Americans live paycheck to paycheck. Without tracking, it’s easy to lose money without realizing where it went.

Skipping emergency savings: Even a modest $500-$1,000 cushion prevents small problems from becoming high-interest credit card debt. Without it, a single car repair or medical bill can spiral.

Ignoring financial planning: Not thinking about saving for retirement until your 40s or 50s means missing decades of compounding. Starting at 25 versus 35 can mean the difference between $1 million and $300,000 at retirement.

Other poor financial decisions to avoid:

Taking payday loans with APRs up to 400%

Chasing hot investment tips without research (90% fail per SEC data)

Not checking free credit reports for errors (20% contain mistakes)

Carrying balances on mutual funds expense accounts unknowingly

Missing employer offers for retirement account matching

Financial education is ongoing. The more financial knowledge you build, the better your decision making becomes.

How to Take Control of Your Finances Starting Today

You don’t need a high income or perfect past decisions to take control of your money right now. Everyone starts somewhere, and starting today puts you ahead of everyone still waiting for the “right time.”

Beginner action checklist for this week:

[ ] Write down your net income and main bills

[ ] Track every expense for 7 days (yes, even coffee)

[ ] Schedule a date to draft a basic monthly budget

[ ] Cancel at least one unused subscription

[ ] Open a separate high-yield savings account if you don’t have one

Immediate steps for better money management:

Set up automatic payments for key bills to avoid late fees

Transfer even $20 to savings today to build momentum

Delete one shopping app from your phone

Set a calendar reminder for a weekly 10-minute financial health check

The best ways to manage personal finances consistently include regular check-ins, automating good habits, and reviewing goals every few months. Life changes, and your plan should change too.

Pick one small step to complete today. Even transferring $20 or tracking your spending builds the habit of taking action with your finances.

Conclusion

The best personal finance tips come down to fundamentals: create a budget, build better spending habits, save consistently, manage debt strategically, and build an emergency fund. These aren’t complicated, but they require consistency and discipline over months and years.

You don’t need to be perfect in any single week. What matters is showing up repeatedly—checking your budget, transferring to savings, making payments on time. Over 5-10 years, these small actions compound into significant financial stability and wealth.

Revisit this guide as your life changes. A new job, a move, or family changes all require updating your money plan. The principles stay the same, but the numbers will shift.

Starting now—even with small steps—is the key. Your future self will thank you for the foundation you build today.

Frequently Asked Questions

How much should I save each month if I’m just starting out?

Beginners can start with $25-$100 per month, or 2-5% of take-home pay. The first priority is usually a starter emergency fund of $500-$1,000. Once that’s established, gradually work toward saving 15-20% of income for long-term goals like a retirement account.

Consistency matters more than the exact amount. Automate what’s affordable and increase it every 3-6 months as you adjust your spending. Even $50/month at 4.5% APY grows to over $10,000 in 10 years.

Is it better to pay off debt or save money first?

A balanced approach works best for most people. Build a small emergency buffer of $500-$1,000 while making at least minimum payments on all debts. This prevents new emergencies from adding to your debt pile.

After your basic emergency fund is in place, prioritize high-interest debt above 20% APR—typically credit cards. These balances grow quickly and cost you more money the longer they sit. Reassess your approach annually based on your job stability and interest rates.

Do I need a high income to follow these personal finance tips?

No. The core habits—tracking expenses, budgeting, saving something, and avoiding high-interest debt—work at any income level. Someone earning $35,000 can apply the same 50/30/20 framework as someone earning $100,000.

Lower incomes require stricter prioritization and mean slower progress toward goals, but the principles remain identical. Focus on controlling what you can: reducing unnecessary expenses, building small savings habits, and avoiding fees that eat into enough money you already have.

How often should I review my budget and financial goals?

For spending, a quick weekly or biweekly review catches problems before they grow. Just 10 minutes checking your account against your budget helps identify if you’re spending less money or more money than planned.

Do a deeper review every 3 months to update categories, adjust savings or debt payments, and revisit short term goals. An annual review updates major assumptions like income changes, housing costs, and long-term plans. Major life events—new job, moving, marriage—should trigger an immediate review.

When should I start investing for retirement?

Once you have a basic emergency fund and high-interest debt under control, start investing for retirement as soon as possible. The power of compounding means that $500/month starting at age 25 grows to over $1 million by 65 at a 7% return—versus roughly $300,000 if you start at 35.

Consider your employer match first—it’s essentially free money, often 50-100% on your contributions up to a limit. If your employer offers a 401(k) match, contribute at least enough to capture it. Then explore individual retirement accounts for additional tax advantaged savings. The stock market involves risk, but historically rewards patient, long-term investors. Don’t let perfect be the enemy of good—starting small beats waiting for the “right time” that never comes.